by Kush Gupta

Jan 27, 2020

SPOTLIGHT

Rebuilding growth through infrastructure spending.

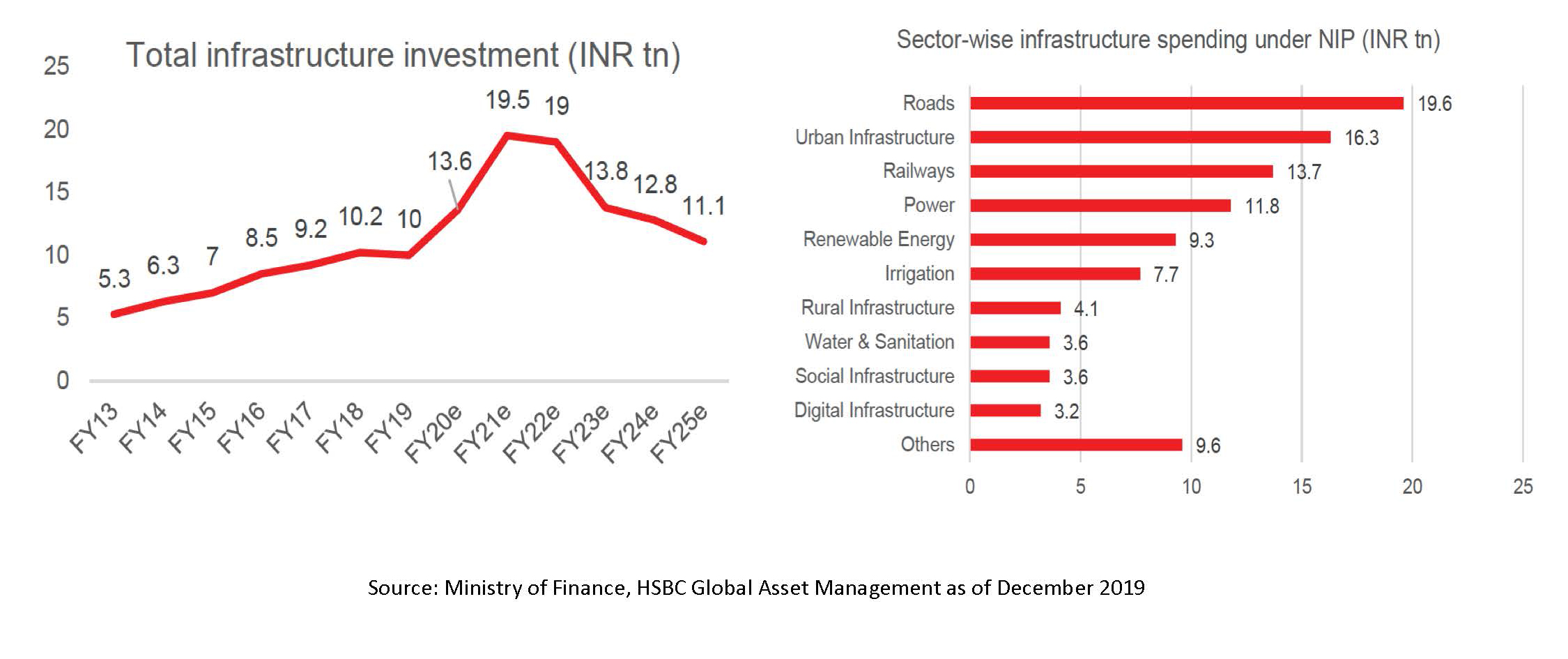

- On 31 December, the government outlined a USD1.4 trillion infrastructure capex plan over the next five years, doubling its spending in the last five years, in a bid to make India a USD5 trillion economy by 2025

- According to data from the government, 43% of the projects are already under various stages of implementation, whereas another ~20% of the projects are in the development stage and the final ~30% are in the conceptualisation stage. This gives the pipeline a fairly high degree of visibility.

- The NIFTY Infrastructure sub-index rose around 2.3% since 31 December, outperforming the broader index.

- The union budget for fiscal year 2021, which will be announced on February 1, is expected to reaffirm the government’s commitment to the infrastructure sector with a focus on key projects such as rural electrification, green energy corridor, dedicated freight corridor and affordable housing.

- The union budget for fiscal year 2021, which will be announced on February 1, is expected to reaffirm the government’s commitment to the infrastructure sector with a focus on key projects such as rural electrification, green energy corridor, dedicated freight corridor and affordable housing.

- With frenzied M&A and investment activity, even during this growth slump; ongoing and planned spending will benefit infrastructure companies across various segments. Despite the challenges in the credit market, key roadway projects have received funding from banks and other financers, and are currently underway.

- There has been meaningful progress on projects of strategic importance to the government such as the privatisation of airports, with six airports already being privatised and a similar number likely to go the same route in the near term

Avg. 3-Year Returns %

Equity Market

- December continued to record net foreign investment inflows into equities, amounting to USD1.0 billion, bringing the yearly total of 2019 to USD14.1 billion. India laid claim to a lion’s share of the flows into EM Asia equities in 2019, accounting for nearly 60% of the USD24 billion total inflows into the region. The strong inflows this year also compare favourably with the outflows seen in 2018.

- Indian equities posted slight gains in the month of December, with the NIFTY Index (INR) up 0.9% and the MSCI India Index (INR) up 1.0%. Compared with the broader universe of emerging markets (MSCIEM) equities, Indian equities (MSCI India) underperformed by 5.6% in USD terms in December. Oneyear forward P/E for MSCI India is around 20x.

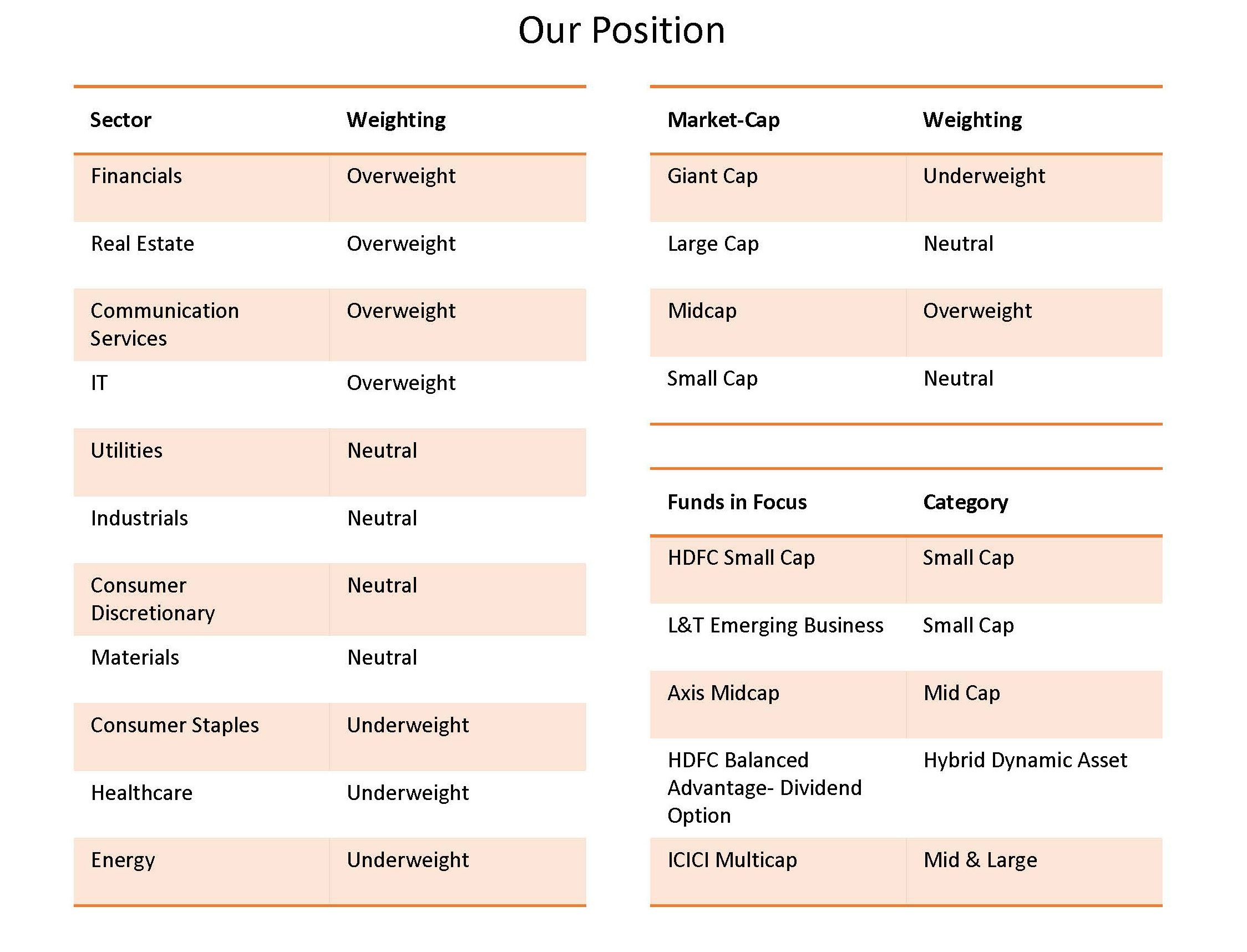

- Oct-Dec quarter earnings are expected to bring some respite to investors amidst the ongoing gradual recovery in the financial sector and the corporate tax cuts announced in 2019.

- Prospects for equity investments in India’s real estate industry look promising, despite developments that negatively impacted the market in 2019, such as the liquidity crunch that began with non-bank financial companies in 2018 and the oversupply situation in the property market.

- India’s manufacturing PMI rose for a second consecutive month in December, helped by an improvement in new orders and employment indexes, after having hit a two-year-low in October.

Debt Market

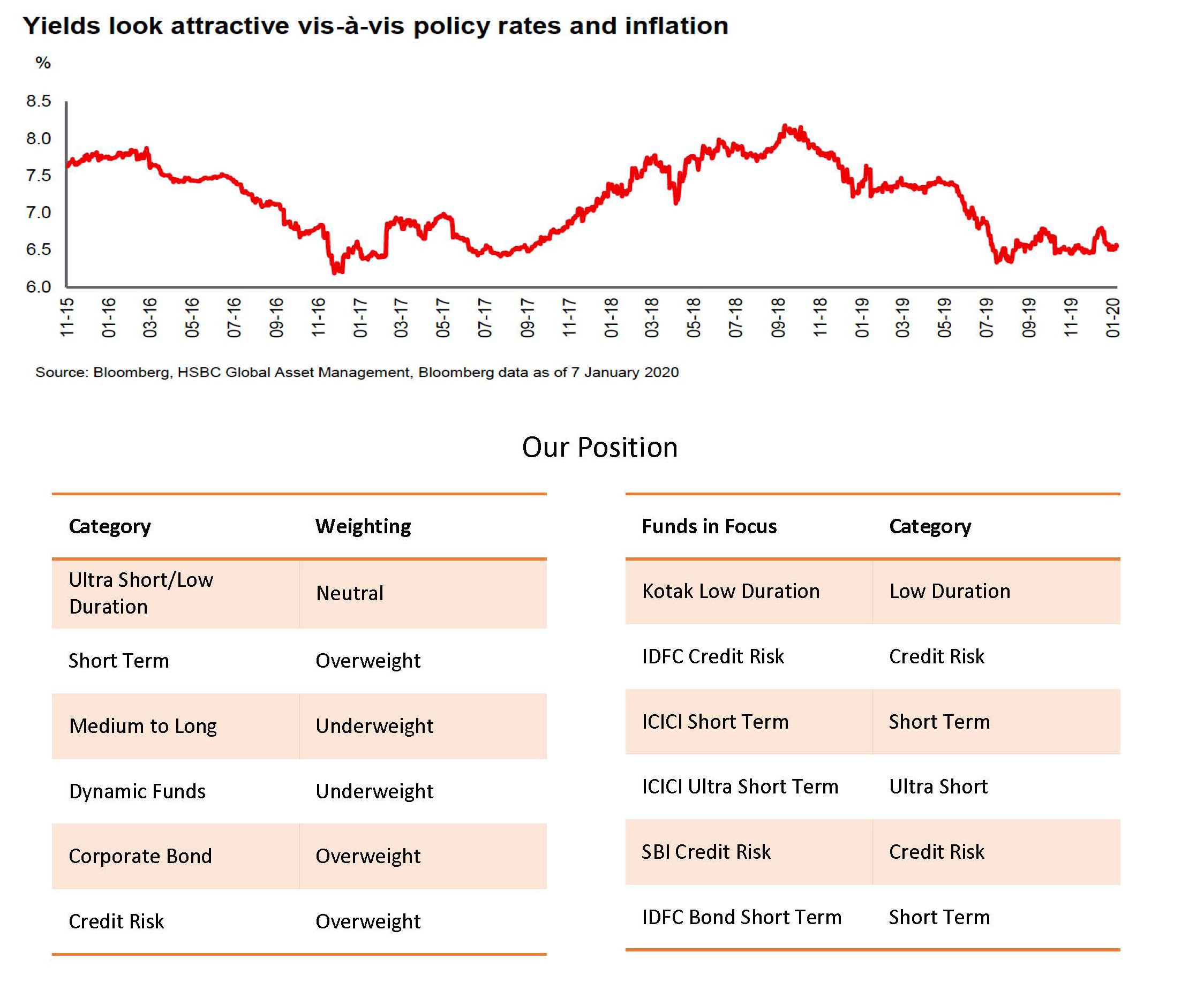

- In 2019, the INR depreciated by 2.26% against the USD. During the year, 2019 saw net inflows from foreign investors of INR 259 billion (USD 3.6 billion)

- The RBI conducted three special “Twist” Open Market Operations, by buying long-dated government securities while simultaneously selling the same amount in short-dated securities. The action is an indication of the RBI’s objective to lower the elevated term premiums, in order to further rate transmission.

- 2019 saw five consecutive policy rate cuts totalling 135bps and the 10-year government bond yields had reached 6.79% in mid-December. RBI is expected to rates by another 40 bps in CY2020 with terminal rate being 4.75%.

- The Finance ministry has made an effort to abate the fear in the minds of bankers from any enquiry resulting out of their normal banking activities. Further, the government has acted to participate with bankers to reduce the lack of trust in the RBI is expected to cut credibility of the underlying assets to lend. The real estate fund is the first of its move.

Why Investments2Go ?

DISCRETION

We understand that your financial affairs are deeply personal and that wealth management relationships are built on a foundation of trust. We take care to maintain discretion and hold your information in strict confidence.

EXPERIENCE

Investments2Go is promoted by a team of over 50 years of combined experienced. Having seen various cycles of boom & bust, we use our knowledge wisely to guide our clients.

A PROVEN PROCESS

An integrated, flexible and time-tested investment process; top-down and bottom-up. A disciplined, opportunistic style open to searching for value everywhere, across all asset classes.

CLIENT SERVICE

We use the breadth of our expertise to to deliver strategies and services aligned with your needs. Recommendations driven solely by your objectives, not by commissions or quotas.